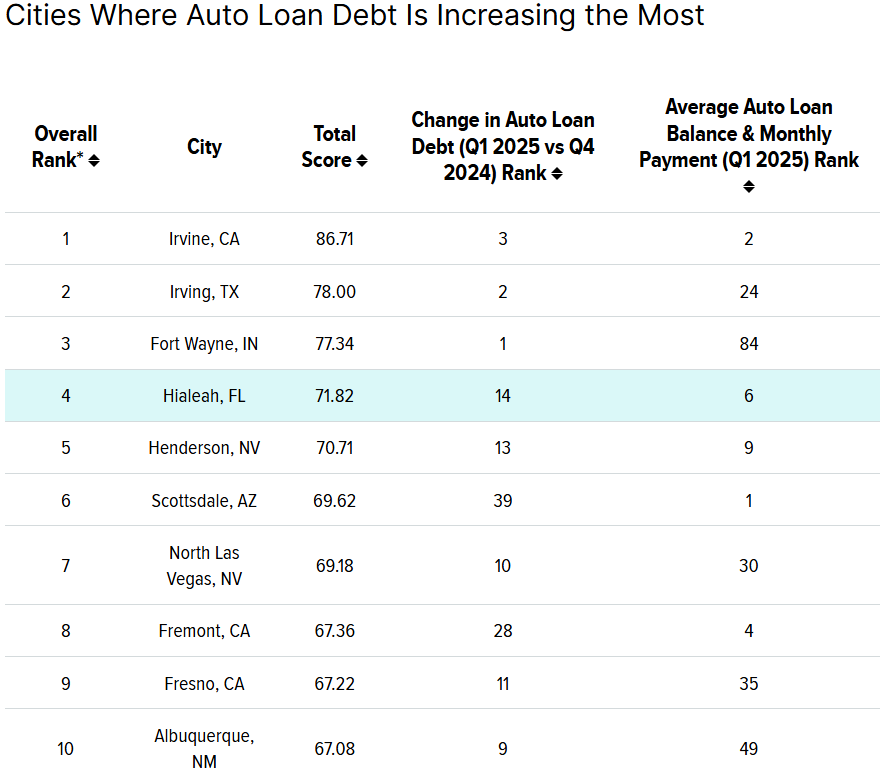

Nearly 1 in 4 vehicle trade-ins toward new car purchases with negative equity carry more than $10,000 in debt, according to Edmunds. The 2025 Q3 data from the online resource for automotive inventory and information, show a growing number of owners are trading in vehicles worth less than what they owe, and the debt they are rolling over is growing.

The latest data reveals:

- More than one in four new vehicle trade-ins are underwater, a four-year high.

- Americans with upside-down car loans owe more than ever.

- Nearly one in three underwater car owners owe between $5,000 and $10,000 in debt — a new record high.

- A record share of underwater car loans are carrying five-figure debt.

Rolling over debt drives higher monthly payments. To highlight the financial effect of rolling negative equity into a new vehicle purchase, Edmunds analysts compared the costs for consumers who financed a new vehicle involving a trade-in with negative equity in Q3 against the industry average for all financed new vehicles. The average monthly payment for buyers who rolled negative equity into a new loan was $907 in Q3, down slightly from Q2’s high of $915 and $140 more than the overall industry average monthly payment of $767.

Click here to learn more.

If you have questions on this topic or are in financial crisis and considering filing for bankruptcy, contact an experienced Miami bankruptcy attorney who can advise you of all of your options. As an experienced CPA as well as a proven bankruptcy lawyer, Timothy Kingcade knows how to help clients take full advantage of the bankruptcy laws to protect their assets and get successful results. Since 1996 Kingcade Garcia McMaken has been helping people from all walks of life build a better tomorrow. Our attorneys help thousands of people every year take advantage of their rights under bankruptcy protection to restart, rebuild and recover. The day you hire our firm; we will contact your creditors to stop the harassment. You can also find useful consumer information on the Kingcade Garcia McMaken website at www.miamibankruptcy.com.