If your business has fallen on hard times, and you can no longer afford to pay your business credit card, you have options. But ignoring the debt will only make matters worse.

In the perfect world, inconsistent cash flow would never be an issue for a small business. But many businesses face it, along with economic uncertainty, and inflation.

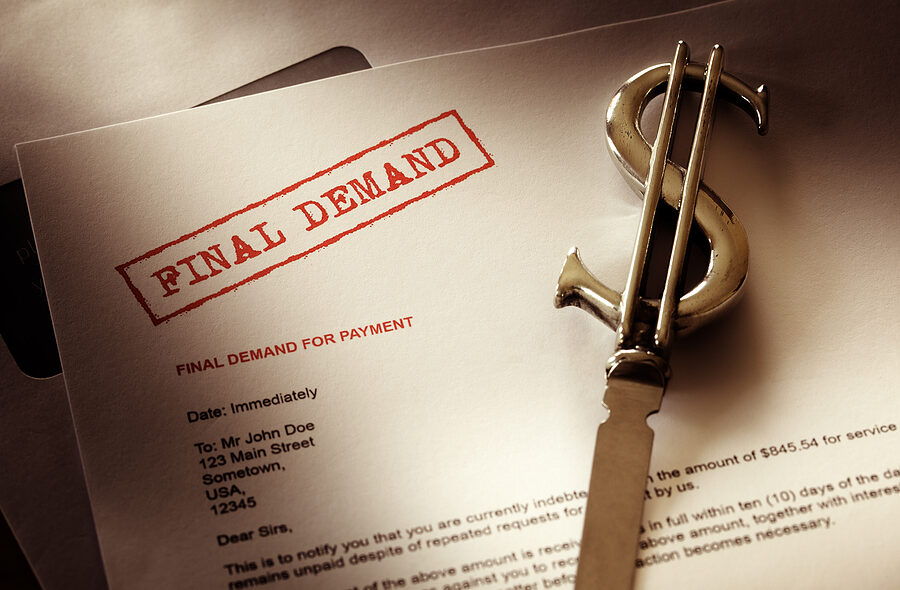

Failing to make payments on a business credit card can result in late fees, higher interest rates, and significantly damage your business and personal credit scores.

Missing payments on your business credit card can trigger a series of penalties and actions. The most severe being legal action against you and your business. Consequences for nonpayment include:

- Late payment fees

- Penalty annual percentage rate, or APR.

- Lower credit scores (both your business and personal)

- Debt collections

- Lawsuits

The personal guarantee on a credit card applies to all business types, including limited liability companies, or LLCs, and corporations. The personal guarantee surpasses any limited liability protections and gives the credit card issuer the explicit right to come to you personally for payment.

The personal guarantee is typically spelled out in the terms and conditions you agree to when signing up for a business credit card. The card issuer checks your personal credit using your social security number to determine how likely you are to repay the debt, when qualifying you for the card.

If you are struggling with business credit debt, contact your card issuer as soon as possible, to minimize penalties and damage to your credit. Your card issuer may be willing to establish a payment arrangement and can inform you of available hardship programs.

As bankruptcy attorneys, we see credit card debt as one of the most common problems facing those with serious financial challenges. If you have questions on this topic or are in financial crisis and considering filing for bankruptcy, contact an experienced Miami bankruptcy attorney who can advise you of all of your options. As an experienced CPA as well as a proven bankruptcy lawyer, Timothy Kingcade knows how to help clients take full advantage of the bankruptcy laws to protect their assets and get successful results. Since 1996 Kingcade Garcia McMaken has been helping people from all walks of life build a better tomorrow. Our attorneys help thousands of people every year take advantage of their rights under bankruptcy protection to restart, rebuild and recover. The day you hire our firm, we will contact your creditors to stop the harassment. You can also find useful consumer information on the Kingcade Garcia McMaken website at www.miamibankruptcy.com.

SOURCE: https://www.nerdwallet.com/article/credit-cards/business-credit-card-personal-guarantee-explained