One of the biggest fears bankruptcy filers have before proceeding with a bankruptcy case is the fear of losing their home. Depending on the type of bankruptcy case being pursued and whether the home has already fallen into default or even foreclosure, it is possible for filers to keep their home during a bankruptcy case.

Tag: Chapter 13 Bankruptcy

What to Expect Before, During and After Filing for Bankruptcy

The process of filing for bankruptcy can seem daunting and unclear for many filers. The uncertainty behind the process often drives the fear of the unknown, which keeps many people from pursuing a bankruptcy case. Pulling back the curtain and knowing what to expect when filing for bankruptcy can help clear up any myths or misconceptions surrounding bankruptcy.

Making the decision to pursue a bankruptcy case is often the thing that holds people back the most. It can be difficult for someone to admit that they need financial help offered through a bankruptcy case. Many see it as admitting failure, which could not be any further from the truth.

6 Steps to Returning to the Business World After Bankruptcy

After a bankruptcy case, the idea of returning to the business world can seem like a pipe dream or a near impossibility. While a bankruptcy case can certainly put a dent in an individual’s credit, it should not hinder that person from successfully starting a business or returning to an already-existing business.

The good news is succeeding in business after a bankruptcy can be and has been done. Many entrepreneurs have gone through personal bankruptcy and come back stronger and better. Several well-known companies, such as General Motors (GM) or Delta Airlines have filed for bankruptcy only to restructure their businesses and rebuild their brands successfully. The following tips can help an individual or business recover after filing bankruptcy.

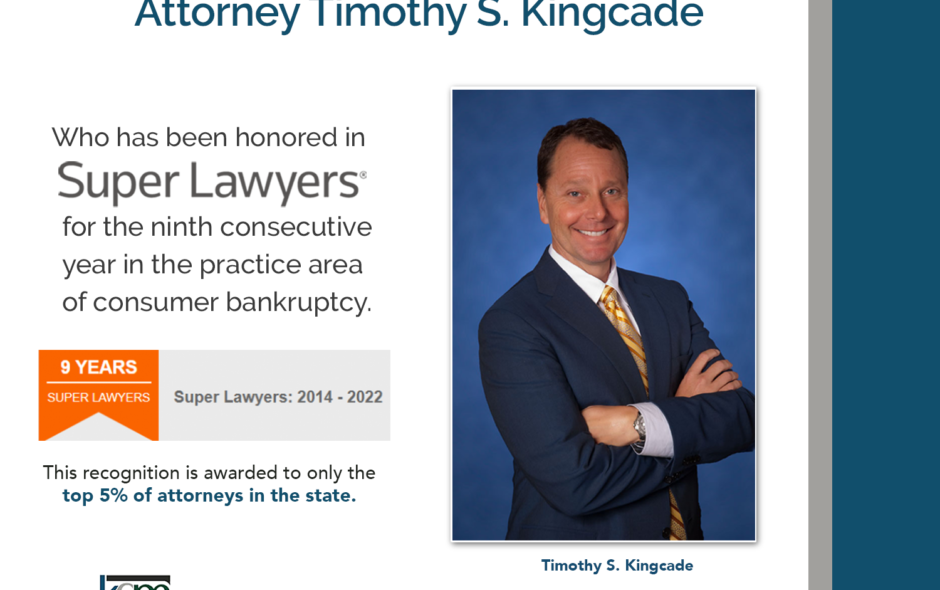

Miami Bankruptcy Attorney Timothy S. Kingcade Named a Florida Super Lawyer 9 Consecutive Years

MIAMI (June 24, 2022)– Managing Shareholder, Timothy S. Kingcade of the Miami-based bankruptcy and foreclosure defense law firm of Kingcade Garcia McMaken has been selected to the 2022 Florida Super Lawyers list. This is the ninth consecutive year Kingcade has been selected to the Florida Super Lawyers list (2014-2022) in the practice area of consumer bankruptcy. The recognition is awarded to only the top 5% of attorneys in the state.

Attorney Kingcade practices exclusively in the field of bankruptcy law, handling Chapter 7 and Chapter 13 filings for the Southern District of Florida. As an experienced CPA and proven bankruptcy attorney, Timothy Kingcade knows how to help clients take full advantage of their rights under the bankruptcy laws to restart, rebuild and recover.

What Debts Are Not Erased in Bankruptcy?

Not all debts can be discharged in a consumer bankruptcy case under the U.S. Bankruptcy Code. These debts will remain with the consumer even at the successful close of the Chapter 7 bankruptcy case. While these debts may remain with the consumer, many of his or her other consumer debts will not. The goal is that with the discharge of other debts, the consumer will have extra money to be able to pay down these non-dischargeable debts.

For the most part, the consumer debts that are discharged include credit card debt, medical bills, past utility bills, personal loans and in some cases student loan debt. Many of these non-dischargeable debts cannot be eliminated due to public policy interests, such as child support.

Do I need a lawyer to file bankruptcy in Florida?

Filing for bankruptcy can be an uncertain and intimidating process. Going through it alone can make the process that much more daunting. While an attorney is not a requirement for filing for bankruptcy, it certainly helps ensure that a bankruptcy case proceeds smoothly.

A bankruptcy attorney will meet with the client first during a consultation to discuss the person’s financial situation to determine whether he or she needs to file for bankruptcy. Occasionally, it can be in the client’s best interest to wait before filing, but he or she may not realize that until talking through the situation with an attorney.

Consumer Debt Reaches a Record-Breaking $15.6 Trillion

Consumer debt hit an all-time high at the end of 2021, reaching a total of $15.6 trillion. According to figures from the Federal Reserve New York district, this figure represents a year-over-year increase of $333 billion during the fourth quarter of 2021, as well as a $1 trillion increase for the entire year.

This quarterly consumer debt increase is the largest one seen since 2007. Looking at it from an annual perspective, this increase is the largest one since 2003.

Latest Bankruptcy Filings Mixed

August and September 2021 bankruptcy filings have been mixed. While certain types of bankruptcy cases have increased, others have gone down, according to data from Epiq’s AACER bankruptcy information services.

According to Epiq, overall bankruptcy filings for all chapters have declined by four percent, with 32,263 new filings made in August 2021 to 30,907 new filings reported in September 2021. Additionally, individual Chapter 7 filings decreased by nine percent between August and September.

Will a Bankruptcy Filing Remove a Vehicle Repossession?

A bankruptcy discharge will relieve the filer of his or her debts, which means that the person can walk away with a clean financial slate. However, a bankruptcy case does not remove all debts from the consumer’s credit report. In fact, certain debts and the legal proceedings associated with them can be difficult to remove, including vehicle repossession.

A consumer bankruptcy case, including Chapters 7 and 13, should remove negative marks on the consumer’s credit report. In a Chapter 7 bankruptcy case this is accomplished by liquidating the consumer’s assets that are not otherwise protected under a bankruptcy exemption and using those funds to pay off the consumer’s debts. Those not paid are then discharged at the end of the bankruptcy. Under a Chapter 13 bankruptcy case, the consumer works with the bankruptcy trustee on a repayment plan that lasts between three to five years. At the end of that time, the remaining debts are discharged from the consumer’s record.

Understanding the Ins and Outs of Bankruptcy

The thought of filing for bankruptcy can conjure up all kinds of emotions. For many, all they know of bankruptcy is what they have heard from others or seen on television advertisements. However, the following information can be helpful in terms of understanding the ins and outs of consumer bankruptcy.

Types of Consumer Bankruptcy.

If a consumer is considering filing for bankruptcy, he or she has two options available. These options are based on the specific chapters within the U.S. Bankruptcy Code. The first option is called Chapter 7 bankruptcy, often referred to as a liquidation bankruptcy. A Chapter 7 case tends to take only several months to complete and involve the filer working with the bankruptcy trustee to sell nonexempt assets and pay off qualifying debts. At the end of the case, the remaining consumer debts held by the filer are discharged. However, to qualify for filing for Chapter 7 bankruptcy, the filer needs to be below a certain income threshold per the bankruptcy court’s means test.

The other option is Chapter 13 bankruptcy, which takes three-to-five years to complete and involves the filer working with the bankruptcy trustee to complete a structured repayment plan on the consumer’s debts. Chapter 13 cases, since they take longer, do cost more in terms of legal fees.