A recent report suggests that bankruptcy filings could soon be on the rise due to the economic hardships many families are facing.

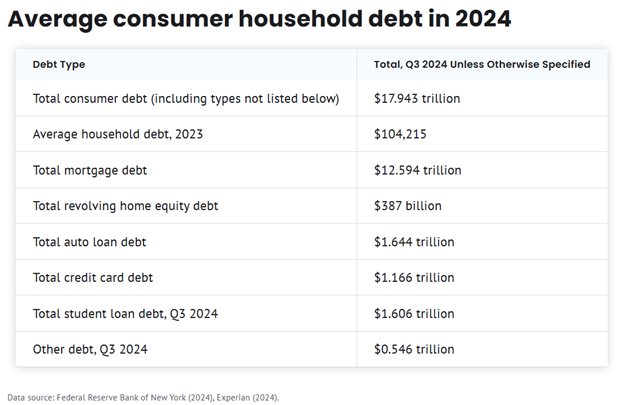

The average American household carries over $105,000 in consumer debt. LegalShield’s Bankruptcy Index suggests that filings this summer could spike to a level not seen since the start of the COVID-19 pandemic.

If you are borrowing to make ends meet every month, bankruptcy can provide you with a way out. There are two paths for individuals considering personal bankruptcy. Filing for Chapter 7 involves liquidating assets to pay off debts, while Chapter 13 allows individuals to keep some assets and restructure their debt.

Certain debts, such as alimony and child support, cannot be discharged in bankruptcy. Student loan debt might be included, but only under specific circumstances. Credit counseling is another option. By following a strict budget and negotiating lower interest rates on outstanding debt, it is possible to get your finances under control.

Click here to read more.

If you have questions on this topic or are in a financial crisis and considering filing for bankruptcy, contact an experienced Miami bankruptcy attorney who can advise you of all of your options. As an experienced CPA as well as a proven bankruptcy lawyer, Timothy Kingcade knows how to help clients take full advantage of the bankruptcy laws to protect their assets and get successful results. Since 1996 Kingcade Garcia McMaken has been helping people from all walks of life build a better tomorrow. Our attorneys’ help thousands of people every year take advantage of their rights under bankruptcy protection to restart, rebuild and recover. The day you hire our firm, we will contact your creditors to stop the harassment. You can also find useful consumer information on the Kingcade Garcia McMaken website at www.miamibankruptcy.com.