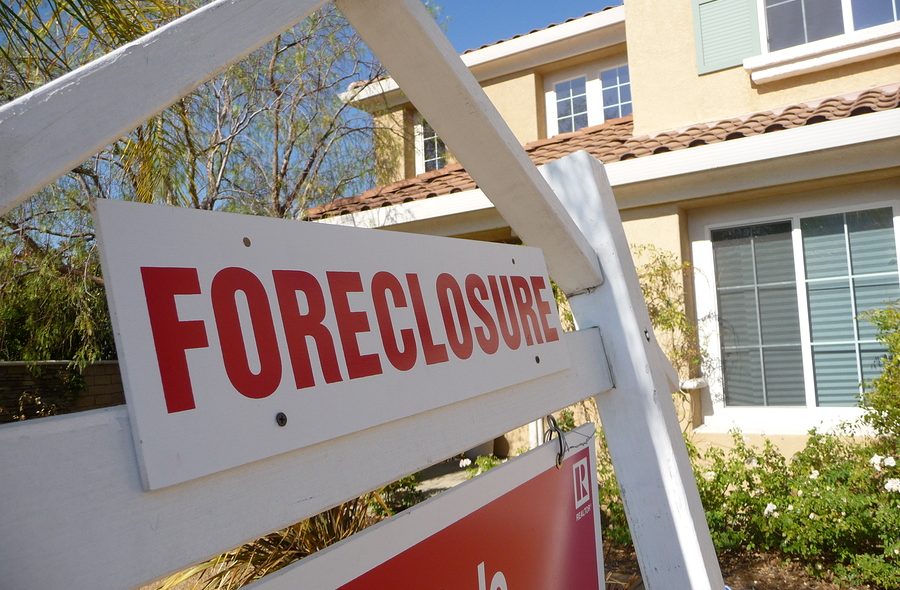

“Zombie foreclosures” occur when a homeowner defaults on their mortgage and moves out of the home before the foreclosure process has been completed. Due to the home being abandoned, signs of dilapidation occur from neglect and lack of maintenance.

If your home is in the middle of foreclosure, it is a good idea to stay put for the time being. Leaving a house does not get you off the hook for bills or legal responsibilities.

Zombie real estate usually happens because homeowners misunderstand the foreclosure process and end up leaving too early.

While the homeowner likely received a “notice of intent to foreclose” (NOI) from the lender – which happens during pre-foreclosure – the lender isn’t required to notify you. As a result, if the foreclosure is canceled without your knowledge, you, the homeowner, still legally own the property and are financially responsible for mortgage payments, insurance, taxes, maintenance, repairs, and other housing-related costs.

Florida has what is called a judicial foreclosure process, which means that every homeowner is entitled to a hearing before the court to determine whether the bank is entitled to foreclose. The most important thing to remember is that the homeowner has rights, and there are ways to slow down the foreclosure process.

If a homeowner has been contacted regarding a zombie debt or old home loan, it is imperative that he or she speak with an attorney as soon as possible. The homeowner should never ignore the legal action, as a default judgment could result.

Choosing the right attorney can make the difference between keeping your home or losing it in foreclosure. A well-qualified Miami foreclosure defense attorney will not only help you keep your home, but they will be able to negotiate a loan that has payments you can afford. Miami foreclosure defense attorney Timothy Kingcade has helped many facing foreclosure alleviate their stress by letting them stay in their homes for at least another year, allowing them to re-organize their lives. If you have any questions on the topic of foreclosure, please feel free to contact me at (305) 285-9100. You can also find useful consumer information on the Kingcade Garcia McMaken website at www.miamibankruptcy.com.