Credit card interest rates are at an all-time high, averaging above 20 percent. The implications of credit card debt are far-reaching. Here are several key insights from Bankrate’s 2025 Credit Card Debt Report.

- 46% of credit cardholders report having a credit card balance. About a quarter (23%) do not think they will ever be able to pay it off.

- Emergency and day-to-day expenses, such as groceries, childcare and utilities, are the most common reasons for credit card debt.

- Credit card debt causes Americans to hold off on important money milestones. Saving for an emergency (34 percent), investing (23 percent) and buying a vehicle (21 percent) are the most likely to be set back.

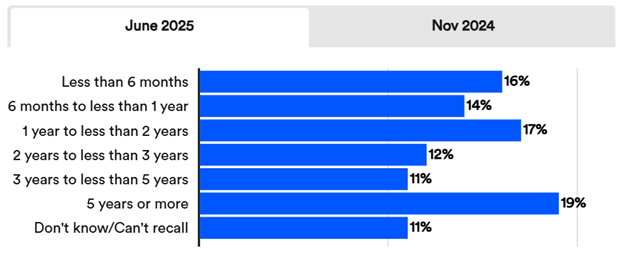

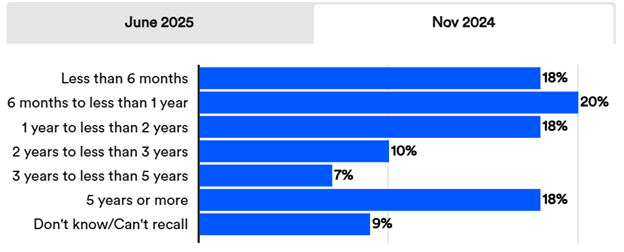

Approximately how long have you been carrying a balance on your credit card(s)?

Note: Among respondents who carry a balance on their credit card(s). Source: Bankrate surveys, June 2-4, 2025, November 13-15, 2024.

Click here to read more.

As bankruptcy attorneys, we see credit card debt as one of the most common problems facing those with serious financial challenges.

Filing for bankruptcy is a viable option for those struggling with insurmountable credit card debt. Chapter 7 is the fastest form of consumer bankruptcy and forgives most unsecured debts like credit card debt, medical bills, and personal loans. There are certain qualifications a consumer must meet in regard to income, assets, and expenses to file for Chapter 7 bankruptcy, which is determined by the bankruptcy means test.

If you have questions on this topic or are in financial crisis and considering filing for bankruptcy, contact an experienced Miami bankruptcy attorney who can advise you of all of your options. As an experienced CPA as well as a proven bankruptcy lawyer, Timothy Kingcade knows how to help clients take full advantage of the bankruptcy laws to protect their assets and get successful results. Since 1996 Kingcade Garcia McMaken has been helping people from all walks of life build a better tomorrow. Our attorneys help thousands of people every year take advantage of their rights under bankruptcy protection to restart, rebuild and recover. The day you hire our firm; we will contact your creditors to stop the harassment. You can also find useful consumer information on the Kingcade Garcia McMaken website at www.miamibankruptcy.com.