Bankruptcy filings have been rising, and personal bankruptcy inquiries have been increasing for those struggling with persistent inflation. Among the options available, Chapter 13 bankruptcy, often referred to as a “wage earner’s plan” or “reorganization bankruptcy,” has become an increasingly common choice for people who need time to catch up on their debts.

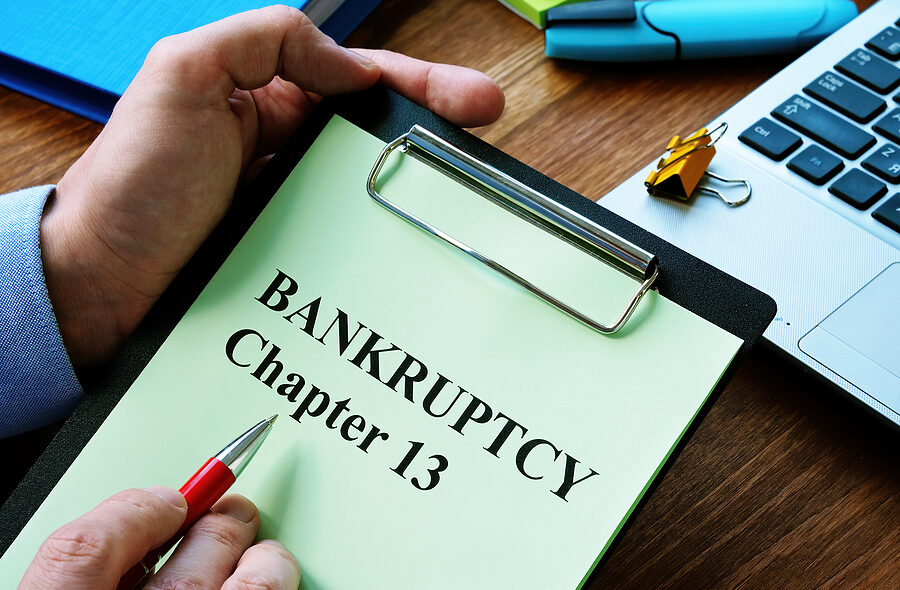

Chapter 13 bankruptcy allows the debtor to keep their property and pay their debts over time, through a court-appointed repayment plan that typically lasts three to five years.

But does filing for Chapter 13 mean you have to give up all your income? Here’s How It Works:

When you file for Chapter 13 bankruptcy, you will submit a detailed budget showing your monthly income and expenses. The bankruptcy court uses this information to determine how much you can realistically afford to pay your creditors each month. Allowed expenses include housing, utilities, food, transportation, insurance, medical care, and other necessary costs. The court follows standardized guidelines for many of these expenses, but there’s flexibility based on a filer’s specific circumstances.

The remaining amount becomes your monthly Chapter 13 payment. This means you keep enough of your income to maintain a basic standard of living while repaying what you can afford with your creditors.

It is also worth noting that not everyone pays back the same percentage of their debt. Some people repay their unsecured creditors in full, while others might pay back only a fraction, sometimes as little as 10% or even less, depending on their disposable income and the value of their assets. The point here is that your payment is based on what you can afford, not on taking everything you earn.

Click here to read more.

If you have questions on this topic or are in a financial crisis and considering filing for bankruptcy, contact an experienced Miami bankruptcy attorney who can assist you and address all of your options. As an experienced CPA as well as a proven bankruptcy lawyer, Timothy Kingcade knows how to help clients take full advantage of the bankruptcy laws to protect their assets and get successful results. Since 1996 Kingcade Garcia McMaken has been helping people from all walks of life build a better tomorrow. Our attorneys’ help thousands of people every year take advantage of their rights under bankruptcy protection to restart, rebuild and recover. The day you hire our firm; we will contact your creditors to stop the harassment. You can also find useful consumer information on the Kingcade Garcia McMaken website at www.miamibankruptcy.com.

Related Resources: