Bankruptcy laws require that the filer be honest and open about his or her financial situation, including disclosing all assets and debts. While no one wants to lose property to pay off creditors, some assets must be sold during the bankruptcy case to pay off the filer’s debts. If a filer actively tries to hide or fails to disclose information in hopes of keeping it from the bankruptcy court, this is called bankruptcy fraud and it can cause your case to be dismissed.

Hiding Assets

Concealing assets is one of the more common forms of bankruptcy fraud. Approximately 70 percent of all cases where some type of fraud was reported involved concealment of assets. It can involve the person simply leaving a certain asset off the list of those reported to the bankruptcy trustee. It can also involve hiding the asset through a fraudulent transfer, including giving the asset to someone else to keep it during the duration of the bankruptcy case, with the intent that the person holding the asset will return it after the case concludes. If this type of fraud is discovered, the filer and the person holding the asset could be held liable for bankruptcy fraud.

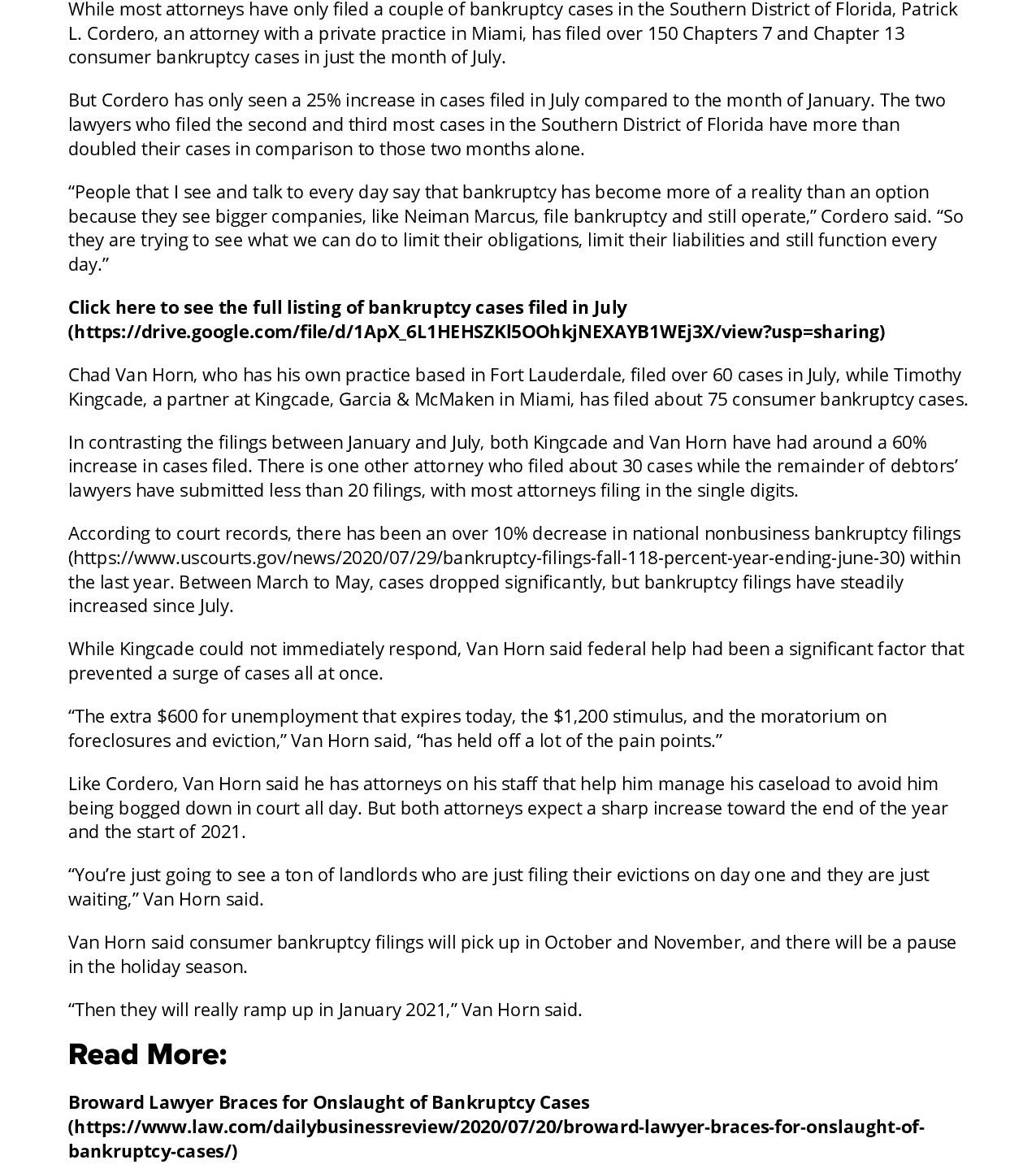

MIAMI – (January 16, 2019) Managing Shareholder, Timothy S. Kingcade of the Miami-based bankruptcy law firm of

MIAMI – (January 16, 2019) Managing Shareholder, Timothy S. Kingcade of the Miami-based bankruptcy law firm of