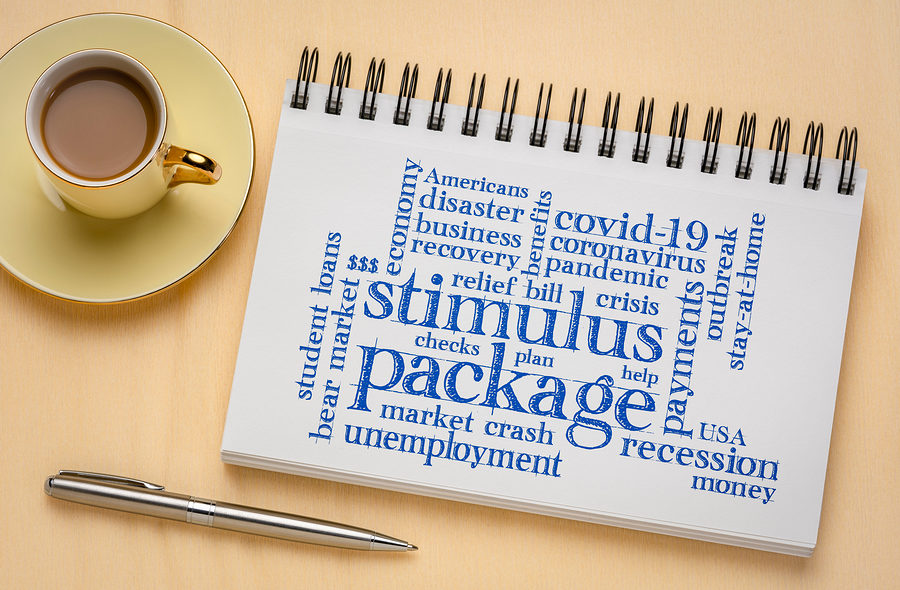

The coronavirus (COVID-19) has hit our nation’s economy hard, with many Americans finding themselves suddenly out of work. Countless small businesses have had to close their doors due to the spread of the coronavirus. Financial assistance is available during the COVID-19 crisis.

A record number of American workers filed for unemployment last week, which totaled 3.28 million people. The biggest form of financial help comes in the form of a recent $2.2 trillion stimulus package passed by Congress just last week. President Trump signed the stimulus bill into law on March 27, 2020.